85% of energy trading professionals reported that hourly shape risk affects their firm. 81% are still managing hourly shape risk with day-ahead positions or OTC trades. These poll results from our joint webinar with ElectronX, highlight how firms are managing short term power risk.

Power markets are changing. Rising renewable penetration is increasing intraday price volatility across US ISOs, creating demand for hourly power futures as a short term risk management tool. New short duration instruments are now available that were not available twelve months ago. The infrastructure required to connect to new venues and meet compliance obligations, however, remains a multi month engineering project at most firms.

During our recent webinar with ElectronX, we polled attendees on four questions covering hourly shape risk, current hedging strategies, venue onboarding timelines, and the infrastructure constraints that drive them. A total of 192 professionals registered for the webinar, including risk managers, compliance officers, and trading heads across energy and commodity markets.

Why hourly power futures matter for short term risk management

Block products treat a range of hours as a single position. When hourly prices diverge from the block average, as they increasingly do with renewable growth, the block position no longer reflects true exposure. Hourly granularity allows firms to measure and manage that deviation directly, which is relevant to short term risk management, forward curve construction, and margin attribution.

Four structural forces are increasing hourly price variance in US power markets.

Unprecedented load growth

US data centres consumed 183 TWh of electricity in 2024, roughly 4% of total consumption, with projections for 2030 standing at 426 TWh. Hyperscalers spent more than $200 billion on infrastructure in 2024. In PJM, data centre capacity growth could reach 31 GW by 2030 against 28.7 GW of new generation the US Energy Information Administration (EIA) expects over the same period. The EIA forecasts overall US power demand will reach 4,283 billion kWh this year, up from 4,097 billion kWh in 2024.

Renewable intermittency

Renewables account for 79% of the 86 GW of new generation capacity planned for 2026. Renewable generation’s share of total US output is expected to grow from 23% in 2024 to 27% in 2026. High solar penetration creates near zero or negative prices at midday followed by steep price ramps as solar output drops in the evening. This pattern, originally documented in CAISO, is now visible across ERCOT, MISO, and PJM. Each hour carries a different price profile as a result.

Battery storage

US battery energy storage reached more than 57 GWh and 28 GW of capacity in 2025, a 29% year-on-year increase. A further 24 GW is expected in 2026, with Texas accounting for 53% of planned development. Battery charge and discharge cycles create price movements that are distinct from the patterns created by generation and demand alone, adding a further source of hourly price variance.

Distributed energy resources

Virtual power plant capacity grew 13.7% in 2025 to 37.5 GW. The US Department of Energy projects VPPs could supply 10 to 20% of US peak demand by 2030. FERC Order 2222 requires ISOs to allow aggregated distributed resources to participate in wholesale markets, increasing the number of variables that influence hourly wholesale prices.

Each of these four forces increases hourly price variance, the core exposure that hourly power futures are designed to manage.

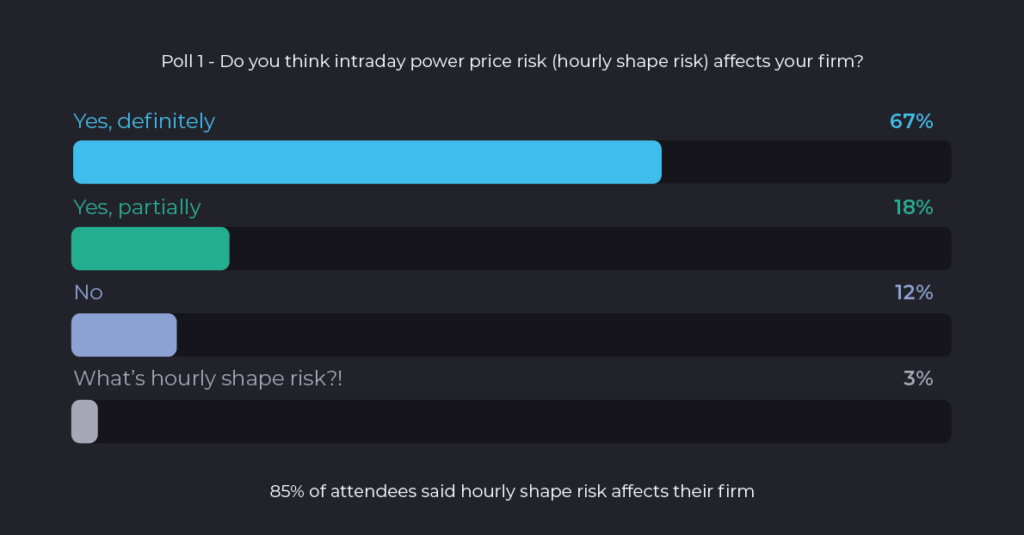

Poll 1: Does hourly shape risk affect your firm?

85% of attendees said hourly shape risk affects their firm, with 67% saying definitely. 12% said it does not apply to them.

Hourly shape risk has a direct P&L consequence. When a firm holds a block position at an average price and real time prices for individual hours within that block deviate materially, up or down, the block position does not reflect the actual hourly exposure. The difference between the block price and each hour’s actual price is either an unhedged gain or an unhedged loss.

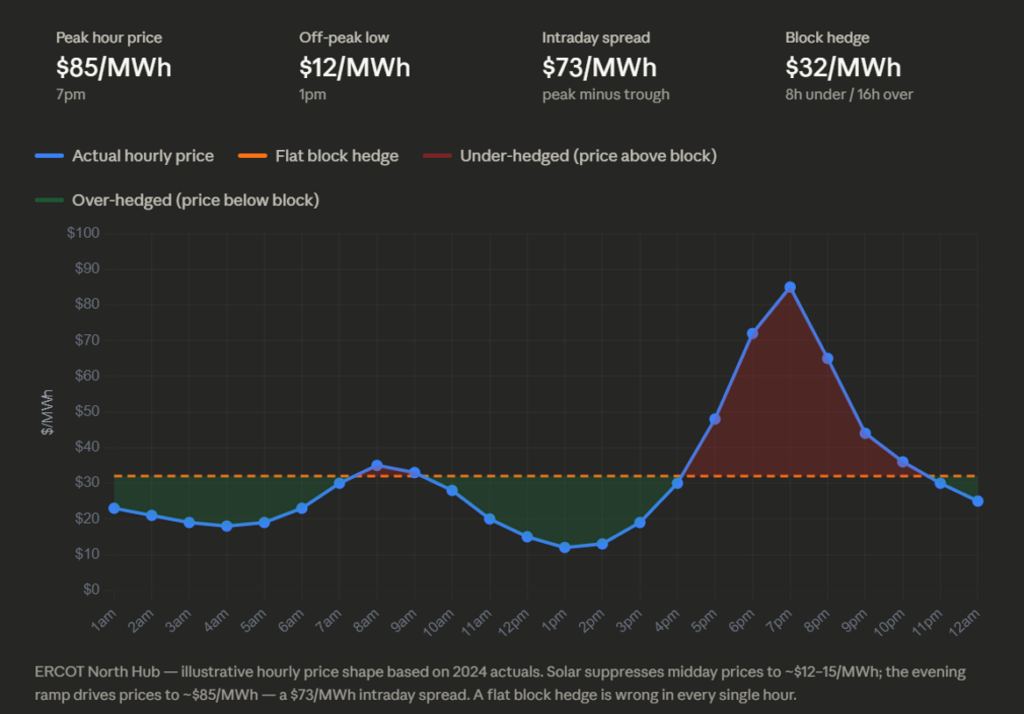

ERCOT illustrates the scale of that exposure, as highlighted in Poll 2 below. The intraday spread between the midday low and the evening peak can exceed $70/MWh on a typical day. A flat block hedge does not capture that movement in either direction.

The same gap affects operational decisions. As a result, forward curves based on block hour averages obscure intraday profitability signals for generation and storage assets. For storage operators, it does not show the optimal hours to charge or discharge. Decisions made from block hour data carry errors that are only visible at settlement, when actual hourly prices are known.

Poll 2: How are firms managing short term power price risk?

58% of respondents use day ahead and balancing positions. 23% rely on OTC or bilateral trades. 15% use hourly futures.

Day ahead contracts fix a price for delivery across a defined period. They do not reflect price differences between individual hours within that period. ERCOT hourly futures data from 2024 illustrates the scale of the exposure. The duck curve makes the exposure visible. In ERCOT, illustrative 2024 data shows a peak hour price of $85/MWh at 7pm, an off peak low of $12/MWh at 1pm, and an intraday spread of $73/MWh. A flat block hedge at $32/MWh is over hedged during the solar suppression period at midday and under hedged during the evening ramp. In no single hour does the block hedge price match the actual hourly price.

OTC and bilateral trades can be structured with more flexibility but typically require credit arrangements, involve intermediaries, and lack the price transparency of exchange traded instruments.

ElectronX hourly bounded futures and binary options settle against verified real time ISO prices at hourly resolution. Bounded futures represent the real time market value of 1 MW of electricity for a specific hour and location. Binary options pay a fixed value based on whether the real time hourly average price settles above or below the day ahead price for the same hour. Settlement uses the simple average of four 15 minute ISO prices per hour. Both products are fully collateralised with no variation margin requirement.

Poll 3: What primarily drives the timeline when adding a new trading venue?

For many energy trading firms, every new exchange connection is a bespoke software build starting from scratch. 65% of respondents said exchange connectivity and data integration, or internal risk system configuration, drives the timeline when their firm adds a new trading venue. 35% cited internal approvals and external provider onboarding.

Internal approval and venue/provider onboarding can be shortened through better governance and faster decision making. Connectivity and risk system configuration cannot. They require engineering work including writing code, building integrations, running tests etc. and that work does not get faster unless the underlying architecture changes.

Energy trading firms that connect to each exchange through a point-to-point integration tightly couple three things: the trading system, the data pipeline, and the exchange’s specific data format. When any one of those three changes i.e., an exchange updates its format, a risk system is upgraded, or a new data feed is added, the change has to be coordinated across all three. What should be a contained fix becomes a multi team engineering project.

In a loosely coupled architecture, the exchange format is handled in a dedicated connectivity layer that sits between the exchange and the trading system. When an exchange updates its format, only the connectivity layer changes. The trading system is never exposed to the exchange specific format and sees no change at all.

The practical consequence is that engineering and IT teams spend a significant portion of their time updating and maintaining existing connections rather than building new ones. The more venues a firm connects to, the worse that ratio becomes.

BroadPeak reduces ElectronX go-live time by 87%

Trade capture must handle ElectronX’s full instrument taxonomy, bounded futures and binary options across ERCOT North, Houston, South, West, Pan, Hub Average, and BUS Average, from day one. Same day expiry products require accurate trade entry within the trading session. Errors in capture on short duration contracts affect position and risk calculations for that session.

End-of-day reconciliation on ElectronX runs directly against exchange reported positions. There is no FCM intermediary. ElectronX’s end-of-day report uses a data model that differs from intermediated venue reporting and needs to be incorporated into existing reconciliation processes before going live.

Market abuse surveillance must be active from the first day of trading. The ElectronX feed contains both trade and order data. Surveillance requires visibility into physical positions alongside financially settled derivatives, including FTRs, to identify patterns that may constitute market abuse. A compliance gap created at go live cannot be closed retrospectively for the period before surveillance was active.

Position limits on ElectronX operate across three tiers: a Single Hour Accountability Level, a Reporting Level, and a Spot Hour Ending Limit. A position limit solution not configured for this structure will not produce accurate real time aggregation from go live.

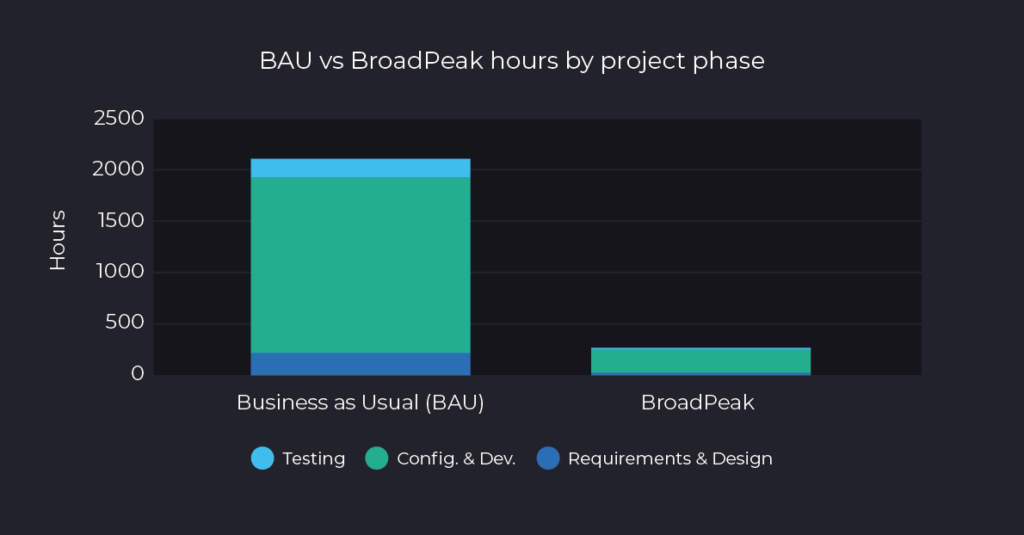

BroadPeak provides prebuilt connectivity and solutions that cover the four capabilities required to go live on ElectronX. Rather than building each component from scratch, firms apply their specific configuration including account details, position limit thresholds, surveillance rules, and reconciliation parameters into BroadPeak’s solutions. BroadPeak’s data shows this reduces the hours required to go live by 87% compared to a custom build, with a corresponding reduction in cost. Ongoing maintenance sits with BroadPeak rather than the client’s internal IT team.

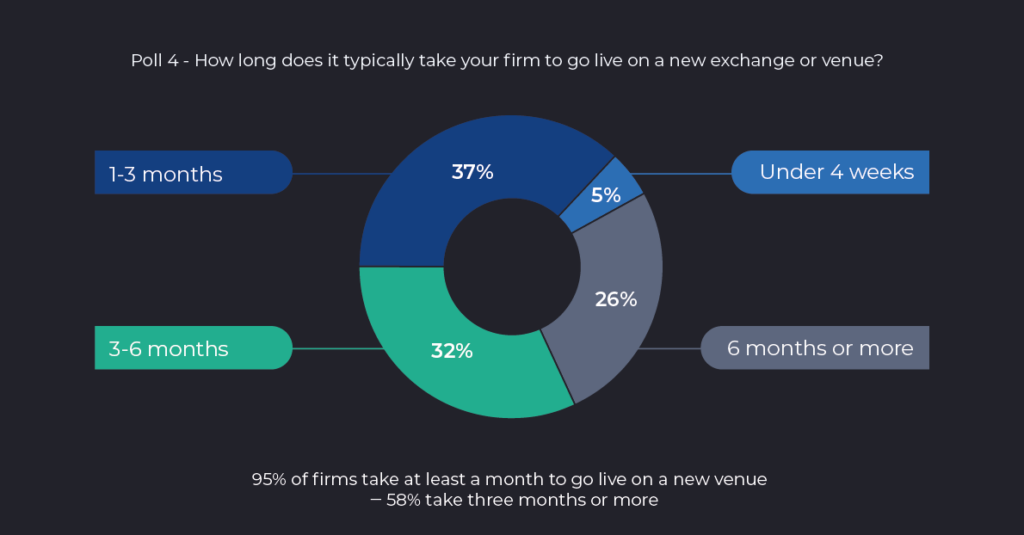

Poll 4: How long does it typically take to go live on a new exchange or venue?

58% of respondents said it takes their firm three months or more to go live on a new exchange. 26% said six months or more. Only 5% said under four weeks.

In a market where ElectronX is expanding across PJM and further ISOs through 2026, every month spent on a connectivity build is a month not trading. Each new ISO ElectronX adds requires firms to build connectivity, configure compliance controls, and update risk systems before they can trade.

BroadPeak maintains prebuilt connectivity across more than 100 global exchanges and brokers. For supported venues, onboarding requires configuration rather than a new build. For firms connecting to ElectronX, that means all four operational requirements, outlined in Poll 3, are covered as part of the same onboarding process.

ElectronX hourly power futures and BroadPeak

ElectronX provides direct access hourly power futures for ERCOT, with no FCM intermediary and no credit requirements. Products are fully collateralised and accessible via GUI and API.

Bounded futures represent the real time market value of 1 MW of electricity for a specific hourly period and hub location. Binary options pay $0 or $100 based on whether real time hourly average price settles above or below the day ahead price for the same hour. Both products settle automatically against verified ISO real time prices using the simple average of four 15 minute prices per hour.

Built for energy and commodity trading firms, BroadPeak connects directly to ElectronX and more than 100 other global exchanges and brokers to deliver clean, structured trade data to your E/CTRM, risk, and analytics platforms.

The strategic implication

The results highlight a gap between the need to manage hourly power risk and firms’ ability to act on it. Firms recognise hourly shape risk as a growing P&L driver, but most continue to manage it using block based instruments. When new hourly power futures become available, many firms cannot connect quickly enough to act from day one.

85% of attendees said hourly shape risk affects their firm, yet 81% are still managing it using day ahead positions or OTC trades. 58% of respondents said it takes their firm three months or more to go live on a new exchange, with 65% citing exchange connectivity and risk system configuration as the primary drivers of that timeline.

Hourly power futures are now available on ElectronX across ERCOT hubs, with PJM and further ISOs following through 2026. The instruments are already in place. For most energy trading firms, the constraint is not access to products, it is the time required to establish connectivity, trade capture, and risk and compliance controls before trading begins.

Hourly Power Futures: frequently asked questions

What are hourly power futures?

Contracts that fix the price of electricity for a specific delivery hour rather than a block of hours. They allow firms to hedge or express a view on the price of individual hours rather than an average across a period.

What is hourly shape risk?

Hourly shape risk is the financial exposure created when actual hourly prices within a trading period deviate from the block average price used to hedge that period. As renewable generation increases hourly price variance, the deviation between block hedges, and actual hourly prices increases.

Why is hourly granularity relevant for short term risk management?

Hourly granularity matters for short term risk management because block positions reflect an average price across multiple hours. When individual hours within that block settle materially above or below the average, the block position does not cover the difference. Hourly positions capture each hour separately, removing that source of unhedged exposure. Hourly positions are also relevant to forward curve construction, where block averages obscure the hour-by-hour price structure that drives actual trading decisions.

Why do firms take months to connect to a new trading venue?

Standard practice requires a custom integration built per venue: a dedicated parser for the exchange data format, data mapping logic, reconciliation routines, and a testing cycle before production. That process typically takes six to twelve months. Prebuilt connectivity infrastructure reduces that timeline by replacing the custom build with configuration against an existing, tested adapter.

How does BroadPeak support firms connecting to ElectronX?

BroadPeak provides prebuilt connectivity and solutions covering trade capture, end-of-day reconciliation, market abuse surveillance, and exchange position limits. In most cases, BroadPeak reduces go-live time by 87% compared to a custom build.