Position limits used to be straightforward. One product, one venue, one limit. You monitored it, you managed it, you moved on. That is no longer the case. Position limit structures and monitoring requirements have fundamentally changed.

Exchanges now apply multiple concurrent constraints to the same product, spanning spot month, single-month, and all-months-combined limits, as well as delivery period controls and cross-venue aggregation requirements. The position limit rules have not just expanded, they have multiplied. The position limit monitoring infrastructure that served you well under the old regime is unlikely to be fit for what comes next.

This is not a back-office reporting obligation. It is a structural shift in how position risk must be captured, calculated, and governed across your entire book.

How position limit structures have changed across ICE, CME, EEX, and LME

ICE, CME, EEX, and LME have each introduced multi-layered limit structures, and the pattern holds across the broader exchange landscape. Regulators and exchanges no longer consider a single aggregate ceiling sufficient to capture market influence risk. They want limits applied at the point of delivery, across the forward curve, and across every venue where the product trades.

Take a natural gas futures contract on ICE. A firm may simultaneously face a spot month limit that activates in the final days before expiry, an all-months-combined limit that aggregates gross long or short exposure across the entire forward curve, and a single-month limit applying to any individual contract month outside the spot period. A single natural gas contract can carry three distinct limit types, and a firm can be compliant on two while breaching the third.

CME applies hard position limits in the spot month under CFTC Part 150, alongside single month and all-months-combined accountability levels for non-spot month positions. The accountability level framework has been in place for many years across the energy complex. Positions above the accountability threshold do not constitute an automatic breach, but they trigger an obligation to provide information to the exchange on request and may result in a direction to reduce.

EEX applies delivery period limits to power products, where the constraint is defined not by calendar month but by the delivery window of the specific contract. That creates a time-varying limit calculation that must track contract maturity dynamically rather than against a fixed calendar.

LME’s prompt date structure introduces its own complexity. Limits apply across a daily prompt calendar that extends out to three months cash and beyond, with different constraint levels applying depending on the prompt date cluster. A firm active across multiple LME metals faces a limit calculation that changes every trading day as prompt dates roll forward.

Cross-venue aggregation adds a further dimension. Where ICE and CME both list contracts referencing the same underlying commodity, exchanges and regulators may require position aggregation across both venues for limit calculation purposes. CFTC rules on aggregation under Part 150 are explicit on this point.

A firm that monitors ICE and CME position limits in isolation, without aggregating to a combined figure, may appear compliant on each venue individually while breaching an applicable combined limit.

What multi-layered position limits mean for risk management

For a Chief Risk Officer at an energy or commodity trading firm, there is one operational question worth asking: how many limit types is your current position limit solution evaluating per product, per venue, and in what time window?

If the answer is one limit per product with end-of-day calculation, you are not monitoring position limits, you are recording them. There is a material difference between a preventive control and a detective one. End-of-day reporting is the latter. Multi-layered limits require intraday calculation at each constraint level, with position data sourced in real time from every exchange where the firm holds an active position. End-of-day reporting identifies breaches after the fact. It does not prevent them.

The aggregation requirement raises a data architecture question. Your solution needs to pull confirmed and unconfirmed positions and OTC positions where applicable, then aggregate to the correct granularity for each limit type. Spot month calculations require the solution to identify which contracts are within the spot period at any given moment and apply a different limit threshold to those positions automatically. That is a materially different calculation from a flat aggregate across all months.

If your risk infrastructure was not built to handle dynamic limit tiers, the gap is structural, not cosmetic.

How multi-layered position limits affect trading desks and intraday monitoring

Desk heads face a practical intraday problem. A trader managing a spread book across multiple contract months may hold a position that sits within the all-months-combined limit but breaches a single-month sub-limit on a specific prompt date. Without real-time visibility across each applicable limit type, the trader has no signal to act on until the breach occurs.

Order management solutions (OMS) that display a single net position figure without disaggregating by limit type are not giving traders the visibility they need to manage within their full limit obligations. The pre-trade limit check must evaluate the proposed order against every applicable limit simultaneously, not just the headline figure. If your OMS pre-trade checks are not configured to that level of granularity, traders are working without a complete picture.

In delivery months, the stakes are higher. Spot month limits are typically set at a level calibrated to physical delivery capacity.

Breaching a spot month limit does not just generate a compliance query. It signals to the exchange that a firm may be accumulating a position it cannot deliver against. The regulatory response is considerably more serious than a standard limit breach.

Position limit monitoring: what compliance and surveillance teams must be able to demonstrate

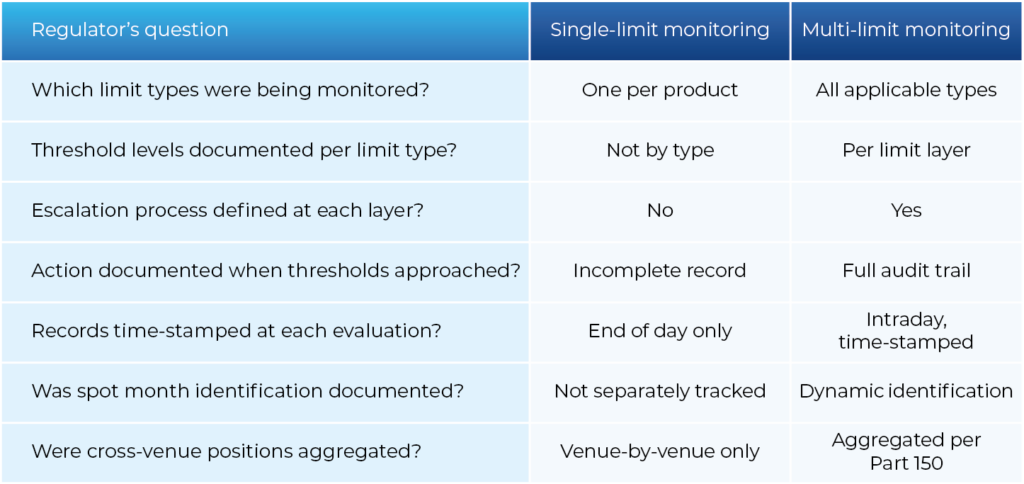

For compliance and surveillance functions, multi-layered limits change the evidentiary standard in an audit or investigation. Regulators and exchanges expect documented evidence that each applicable limit type was being monitored, that escalation thresholds were defined at each layer, and that the firm can demonstrate what action was taken when a threshold was approached.

That documentation requirement applies per limit type, not just to the headline figure. If a surveillance solution captures a single net position per product and runs it against one limit, the compliance evidence trail is incomplete. In an ICE Market Surveillance investigation or a CFTC inquiry under Part 150, the question will be specific: which limit types were being monitored, what were the threshold levels, and when were they breached or approached? The answer needs to be granular and time-stamped.

Legacy position limit monitoring solutions were designed around a single limit per product. The data model, the calculation engine, and the reporting layer all reflect that assumption. Retrofitting multi-limit capability onto that architecture is technically possible but operationally fragile. It typically produces a combination of custom scripts, manual overlays, and parallel spreadsheet processes that introduce calculation risk and version control problems.

The specific capabilities a position limit monitoring solution needs to handle the current exchange environment are: native support for multiple concurrent limit types per product, dynamic spot month identification based on contract maturity, real-time aggregation across venues including OTC where applicable, pre-trade limit checking against all constraint layers simultaneously, and an audit trail that records position figures and limit calculations at each evaluation point.

Firms that have not tested their solutions against that specification explicitly should do so. The testing method is straightforward: take a product with a known multi-layered limit structure, construct a position that is compliant on the aggregate but approaches a sub-limit, and verify whether your solution generates the correct signal at the correct threshold.

The case for real-time position limit monitoring

The direction from exchanges and regulators is toward more granularity in limit structures, not less. New venues entering power, gas, and metals markets are adopting layered constraint models from launch. The CFTC’s Part 150 rulemaking and the FCA’s transfer of position limit oversight to ICE Futures Europe and LME under PS25/1 both point toward a more rigorous compliance environment, not a lighter one.

Energy and commodity trading firms that build position limit monitoring infrastructure capable of handling multiple concurrent limits across venues gain a practical advantage. The ability to trade actively across spot and forward periods with real-time visibility at every constraint level means faster, more confident position management. It also means a defensible compliance record if and when a regulator asks.

The firms that treat position limit monitoring as a single-figure calculation will continue to operate until the gap becomes visible. In this environment, visible gaps tend to surface at the worst possible moment.

How BroadPeak handles position limit complexity

BroadPeak provides real-time position limit monitoring for energy and commodity trading firms across multiple exchanges and jurisdictions. Unlike most monitoring approaches that rely on static reference tables or manual data entry, BroadPeak’s Position Limits solution ingests authoritative limit data directly from global exchanges in near real time, processing around two million pieces of position limit reference data daily. Limits vary by product, expiry, contract type, and participant type, and they change frequently.

BroadPeak’s Position Limits solution captures those changes as they happen. The solution is built to handle the limit logic other position limit monitoring solutions do not address: diminishing factors that reduce position value as the spot month approaches, parent-child product groupings that reflect how exchanges measure total exposure, and futures equivalent position calculations that unify futures and options into a single delta-based figure aligned with exchange rules.

Do you know where your multi-limit monitoring falls short?

Most firms do not know where their multi-limit monitoring falls short until a breach makes it visible. BroadPeak’s complimentary Position Limit System Readiness Diagnostic gives firms a structured assessment of their current position limit monitoring against every applicable limit type across their traded venues. The output is specific: where coverage is complete, where it is not, and what needs to change.

Frequently asked questions

What are multi-layered position limits?

Multi-layered position limits are multiple concurrent constraints applied to the same futures or derivatives contract. A single product may carry a spot month limit alongside single-month and all-months-combined thresholds, each triggering different obligations and levels of scrutiny. These controls operate concurrently, and a breach or trigger in one does not necessarily imply a breach in another.

Which exchanges apply multi-layered position limits?

ICE Futures Europe, CME, EEX, and LME all apply layered limit structures across their energy, commodity, and metals products. ICE and CME apply spot month and all-months-combined limits. EEX applies delivery period limits to power contracts. LME applies limits across a rolling daily prompt calendar.

What is cross-venue position aggregation under CFTC Part 150?

CFTC Part 150 requires firms to aggregate positions held across multiple venues where contracts reference the same underlying product. A firm monitoring ICE and CME positions in isolation may appear compliant on each venue individually while breaching an applicable combined limit.

How often should position limits be calculated?

Multi-layered position limits require intraday calculation at each constraint level. End-of-day reporting identifies breaches after the fact but does not prevent them. Spot month limits in particular require real-time monitoring given the regulatory consequences of breach during the delivery period.

What happens if a firm breaches a spot month position limit?

Breaching a spot month limit signals to the exchange that a firm may be accumulating a position it cannot deliver against. The regulatory response is considerably more serious than a standard limit breach and may include a direction to reduce the position, an exchange investigation, or referral to the relevant regulator.